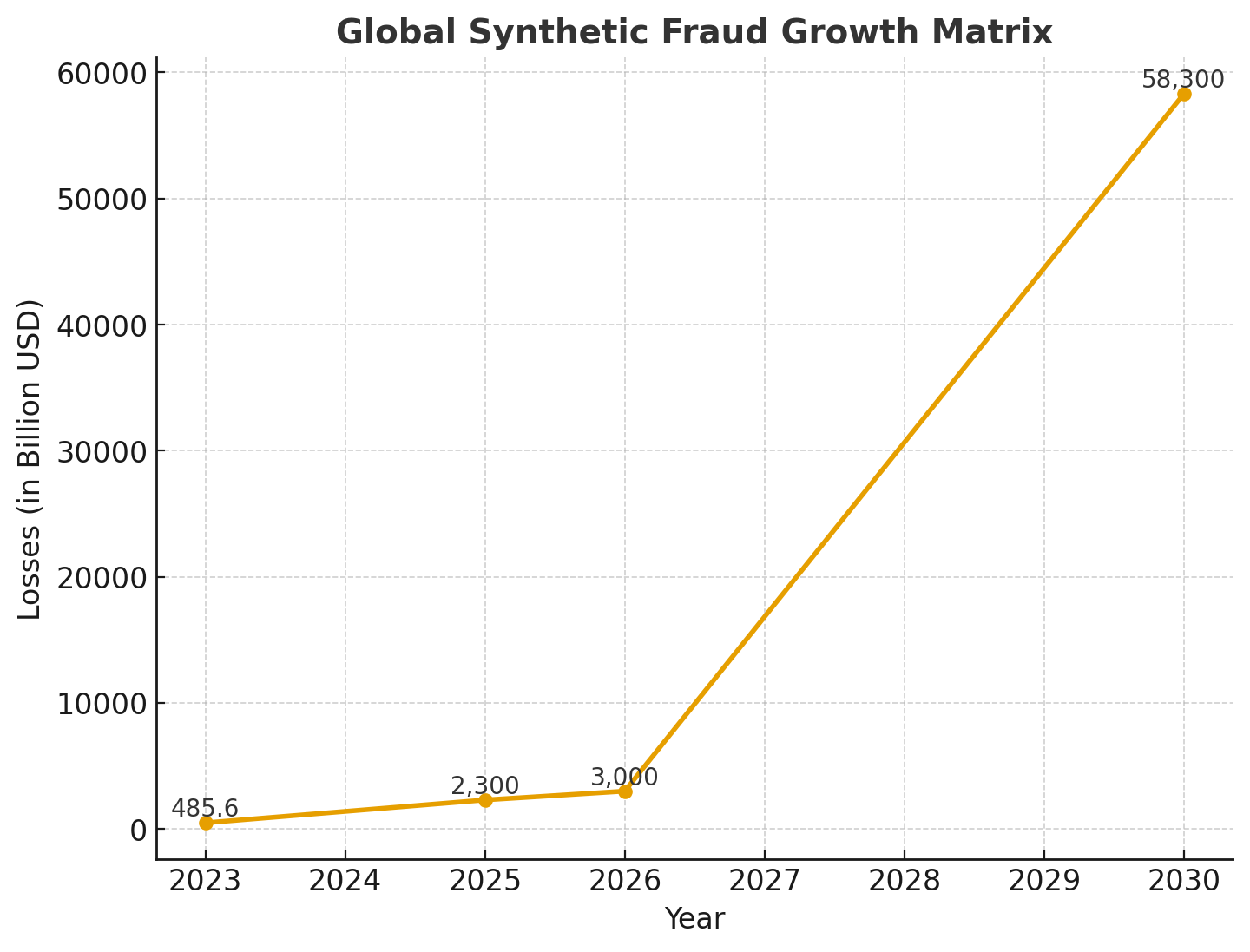

Synthetic fraud—blending stolen and fake identity data into fictitious personas—is harder to detect than traditional fraud and exploits legitimate systems to build credibility. With cases rising worldwide, it is projected to surpass $3 trillion by 2026, making it one of the gravest financial crime threats.

AI-driven synthetic fraud is eroding trust in financial systems by bypassing traditional verification. Institutions must adopt dynamic, AI-powered defenses to preserve credibility, as global fraud losses hit $485.6 billion in 2023, with synthetic fraud emerging as a major driver due to its scale and sophistication.

Countries Most Affected

A report says, Synthetic identity fraud is noted as a growing concern, with losses in the U.S. alone projected to reach $23 billion by 2030.

Juniper Research forecasts global fraud losses for financial institutions to rise from $23 billion in 2025 to $58.3 billion by 2030, driven largely by synthetic identity fraud, which uses a mix of real, stolen, and fake information to create fraudulent personas. Another source, the ACFE Insights Blog, mentions Interpol's estimate of $3 trillion in annual global cyberfraud profits.

(Global synthetic fraud losses are projected to surge from $485.6B in 2023 to $3T by 2026. Financial institution fraud alone is expected to hit $58.3B by 2030)

Impact Across Industries:

The Scale of the Threat

According to industry forecasts, global synthetic fraud losses are expected to surpass $3 trillion by 2026, threatening trust in financial systems and digital platforms alike.

Solutions from FaceOff AI ( FO AI)

Directly targets fictitious personas by orchestrating continuous behavioral biometrics (e.g., gaze, micromotions, device hygiene). It monitors for "build-up" patterns—like gradual credit building—using LSTM for temporal inconsistency detection, preventing strikes before they occur.

Tips to Spot & Mitigate Synthetic Fraud

1. Look for inconsistencies in documents (mismatched SSN, Aadhaar, or phone details).

2. Monitor behavioral biometrics to spot unusual user interactions.

3. Deploy deepfake detection to prevent impersonation during digital onboarding.

4. Use federated learning models for cross-bank fraud intelligence without compromising data privacy.

5. Educate users on scams exploiting deepfakes, gaming impersonation, and digital lending traps.

Synthetic fraud often builds "sleeper" identities over time, exploiting gaps in static checks. FaceOff's orchestration counters this by monitoring dynamic, hard-to-fake cues, detecting inconsistencies that reveal fabrication.

FaceOff (FO AI) tackles synthetic fraud by leveraging its Adaptive Cognito Engine (ACE) as the central orchestrator. ACE fuses eight core AI models with Agentic RAG, Federated Learning, and synthetic fraud detection modules to integrate multimodal data, enable real-time analysis, ensure continuous authentication, and deliver adaptive trust scoring.

ACE acts as FaceOff’s “brain,” orchestrating multimodal inputs across onboarding, KYC, and transactions. Powered by Agentic AI and RAG, it cross-validates signals to prevent siloed detection, reducing false positives by 20–40% in high-risk cases like digital lending and UPI payments.

Key orchestration principles:

# Modular Integration: 8 core models feed ACE; Agentic RAG adds reasoning with threat intelligence.

# Federated Learning: Decentralized model training ensures privacy (DPDP/GDPR) while spotting cross-border fraud.

# Real-Time Scalability: API-first, cloud/edge ready, delivers results in 2–3 seconds.

# Explainable Outputs: Trust score (1–10) with clear breakdowns for risk-based decisions.

Synthetic fraud is no longer a niche threat—it is a systemic global risk. Combating it requires advanced behavioral biometrics, liveness detection, AI-powered trust systems, and global collaboration across regulators, banks, and digital ecosystems. Without decisive action, financial crime will continue to escalate, undermining digital trust.

Overall, FaceOff's orchestration transforms fraud detection from reactive to proactive, leveraging AI's strengths against its own misuse in synthetic fraud. By fusing dynamic signals and collaborative learning, it restores trust in digital ecosystems amid projections of $3T global losses by 2026.